DURHAM, N.C. — After a three-year pause, federal student loan payments have officially restarted. According to the Center for Responsible Lending, a North Carolina-based nonprofit, as of March 31, 2023, more than 1.3 million North Carolinians had student loan debt totaling more than $51 billion.

According to CRL, 55% of North Carolina college graduates had student loan debt in 2019 to 2020 and the average debt amount was $29,681.

Experts say it’s common for borrowers to feel overwhelmed as these payments restart, but there are resources to help.

“Almost 1 in 4 borrowers were getting ready to be in default or at risk already. About 2.6 million borrowers were already in this risk factor. So what we want to make sure this on-ramp process is safe for borrowers. We don't want to widen that gap,” said Jaylon Herbin, the director of Federal Campaigns for CRL.

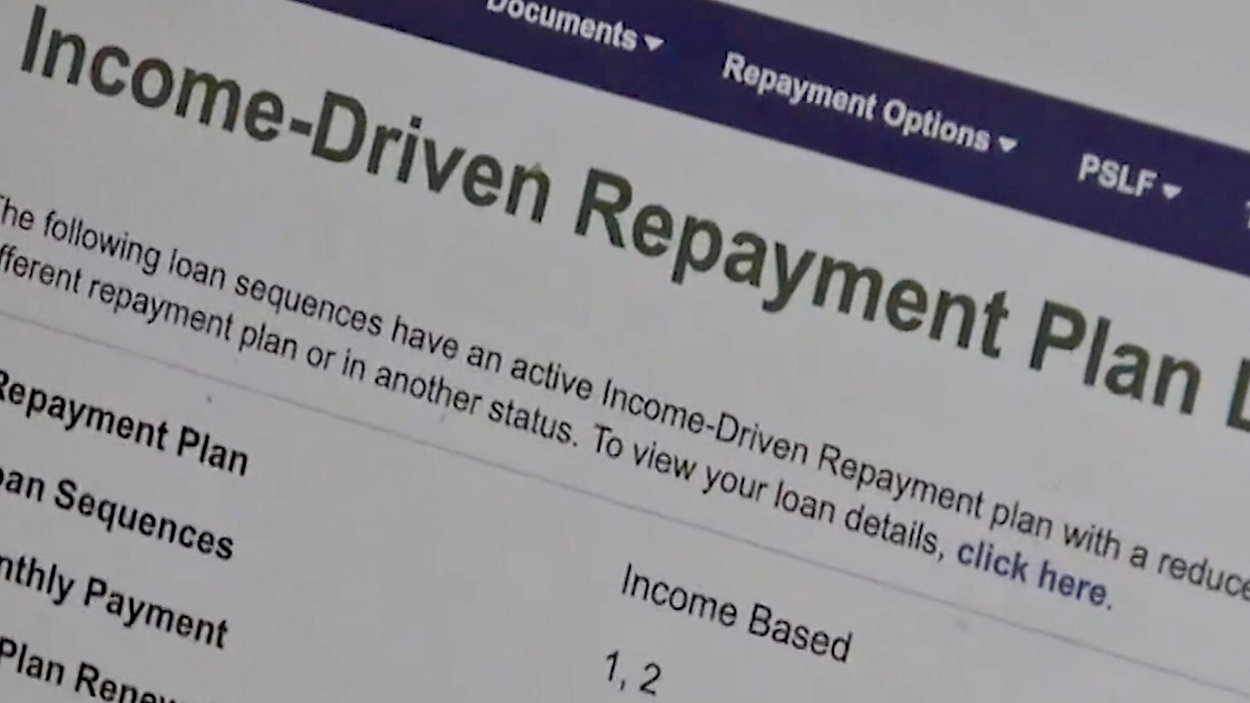

Herbin says there are things borrowers can do to ease the stress of these payments. First, know your loan servicer because many of them changed during the pandemic. Second, confirm your balance, interest rate and monthly payment. That information is available in your online account. Third, do research and figure out what programs you may qualify for, including potential loan forgiveness programs for people in public service. Lastly, see if an income-driven repayment plan would help your situation.

“There is a sense of we need help right now. We've seen the polls. A lot of borrowers strongly support having student debt cancellation and broad-based student debt cancellation at that. So I think that's something that we are going to continue to advocate for, to continue to fight for,” Herbin said.

Herbin says the average borrower could save as much as $400 a month on payments with the new income-driven repayment option.

Herbin says there’s also a 12-month grace period to help borrowers adjust to this change. Experts say you can and should make your monthly payments. However, if you don’t, you won’t be at risk of default, and it won’t hurt your credit score, but interest will accrue whether you make payments or not.